$1000 Installment Loans Explained: Flexible Borrowing Made Simple

- Installment Loans

A sudden expense—like a car repair, utility bill, or unexpected medical cost—can throw your entire budget off balance. For many households, borrowing just enough to cover the gap—without overextending—is a smart and necessary move. In fact, according to recent financial surveys, nearly 40% of Americans say they wouldn’t be able to afford a $1000 emergency without borrowing or dipping into savings.

That’s where $1000 installment loans come in. These loans offer a fixed borrowing amount and allow you to repay it in equal monthly installments over a set period. You don’t need to put up collateral, and you won’t be expected to repay everything in a single lump sum. Instead, installment loans give you predictable payments and a more structured path toward financial recovery.

Let’s say your car breaks down and the repair bill is $980. A $1000 installment loan can help you cover the cost and spread the repayment over a few months—making it easier to stay on track financially without relying on high-interest credit cards or payday loans.

Short-term installment loans like these are a common option for people looking to manage smaller expenses responsibly while maintaining control over their monthly budget. In this guide, we’ll break down how $1000 installment loans work, who they’re designed for, how to qualify, and what to expect from the repayment terms—so you can make a confident, informed decision that fits your situation.

Understanding $1000 Installment Loans: The Basics

A $1000 installment loan is a short-term borrowing option that allows you to receive a fixed amount of money—typically $1000—and repay it over time through scheduled, equal payments. Unlike payday loans, which often require full repayment by your next paycheck, installment loans offer a more manageable solution with consistent monthly or biweekly installments.

These loans are typically unsecured, meaning you don’t need to provide any collateral like a vehicle or property. Once approved, the funds are deposited directly into your bank account. From there, you’ll begin repaying the loan in set amounts over an agreed term—often between a few weeks and a few months—depending on the lender’s policies and your ability to repay.

Because the payment schedule and terms are clearly defined up front, $1000 installment loans are easier to budget for. You’ll know exactly how much you owe, when it’s due, and how long it will take to repay the full amount. That transparency is what makes them a popular alternative to more unpredictable or high-interest credit options.

These loans are commonly used for expenses like:

- Emergency car repairs

- Overdue utility bills

- Rent shortages

- Unexpected medical costs

Whether you’re managing a one-time emergency or need temporary financial relief, installment loans can provide structure and flexibility without long-term debt.

Good Expert Tip

Before accepting a loan offer, always review the repayment schedule and total cost of the loan—not just the monthly payment. Responsible borrowing starts with understanding the full picture.

Who Can Benefit from a $1000 Installment Loan?

A $1000 installment loan can be a useful financial tool for a wide range of individuals—especially those who need a modest amount of money to manage an urgent or unplanned expense. Because of their flexible terms and straightforward repayment structure, these loans are often ideal for people who want short-term financial relief without long-term commitments.

Here are a few common scenarios where a $1000 installment loan may be helpful:

- Workers with irregular income: Gig workers, freelancers, and seasonal employees often face cash flow gaps. A fixed loan with predictable payments can help cover expenses during slower periods.

- Households with tight budgets: Families living paycheck to paycheck may not have savings for unexpected costs like car repairs or medical bills.

- People rebuilding credit: Many lenders accept applicants with fair or poor credit, focusing instead on proof of steady income. This makes installment loans more accessible than traditional bank loans.

- Renters facing a temporary shortfall: A $1000 loan may be just enough to cover a rent gap and avoid late fees or eviction.

- Young adults managing new financial responsibilities: First-time borrowers may use installment loans to manage their budgets while building credit responsibly.

What sets these loans apart is their balance between accessibility and structure. Instead of requiring a perfect credit score, most direct lenders will look at your current financial stability—such as consistent income and a valid checking account. This makes them suitable for borrowers who may not qualify for traditional credit options but still want to borrow responsibly.

Good Expert Tip

If your income is steady and you can commit to a fixed payment schedule, a $1000 installment loan can serve as a smart bridge between unexpected expenses and your next paycheck—without overextending your budget.

How to Qualify for a $1000 Installment Loan

Qualifying for a $1000 installment loan is generally more straightforward than applying for a traditional bank loan. Many direct lenders focus on your current ability to repay rather than relying solely on your credit score. This makes installment loans a practical choice for individuals with limited credit history or past financial challenges.

While each lender sets its own criteria, most require a few basic qualifications:

- Proof of income: Whether you’re employed, self-employed, or receive consistent benefits, you’ll need to show that you have a steady source of income.

- Active checking account: Lenders typically deposit funds and collect repayments through your bank account, so having an active account is essential.

- Government-issued ID: You’ll need to verify your identity with a valid driver’s license or state-issued ID.

- Age requirement: You must be at least 18 years old to apply.

- Contact information: A valid phone number and email address are often required for communication and verification.

| Requirement | Description | Why It Matters |

|---|---|---|

| Proof of Income | Recent pay stubs, bank statements, or benefits letters | Shows ability to repay the loan |

| State-Issued ID | Valid driver’s license or government-issued identification | Verifies your identity |

| Active Checking Account | Must be in your name for deposits and automatic payments | Required for fund transfer and debits |

| Age Requirement | Must be 18 years or older | Legal borrowing age |

| Contact Information | Valid phone number and email address | Enables communication and verification |

Most direct lenders require these basic items to assess your eligibility and process your application securely.

Some lenders conduct soft credit checks, which do not affect your credit score. This allows them to review your borrowing history and assess your risk without triggering a negative impact. Others may focus entirely on your income and current financial obligations, especially if they specialize in loans for bad credit or nontraditional borrowers.

Meeting these basic requirements doesn’t guarantee approval, but it does improve your chances—especially if you can demonstrate reliable income and the ability to make regular payments.

Good Expert Tip

Before you apply, gather your documents—such as recent pay stubs or bank statements—and double-check your application for accuracy. Being prepared can speed up approval and help you avoid delays.

What to Expect in the Repayment Terms

One of the key benefits of a $1000 installment loan is the structured repayment plan. Instead of repaying the full amount in a single lump sum—as with payday loans—you repay the loan in fixed, predictable installments over a set period. This structure makes it easier to manage your monthly budget and plan ahead.

1. Repayment Schedule and Frequency

Most lenders offer biweekly or monthly repayment options, depending on your income schedule. For example, if you receive a paycheck every two weeks, you may prefer a biweekly plan that aligns with your cash flow. Monthly plans, on the other hand, are useful for those with more stable, salaried income.

Typical loan terms range from 2 to 6 months, although some lenders may offer shorter or slightly longer durations. Because the loan amount is modest—$1000—repayment periods are usually short-term to keep interest costs in check.

2. Fixed Payments

Each installment includes a portion of the principal and interest. This means your payments remain consistent throughout the life of the loan, with no surprises or balloon payments at the end. Fixed payments make it easier to maintain control of your budget and avoid falling behind.

For example:

- A 3-month loan of $1000 might result in 3 equal monthly payments of approximately $350–$380, depending on the interest rate and fees.

- A 6-month plan might lower those payments to around $180–$200, but with slightly more total interest paid over time.

These are just illustrative ranges—exact repayment amounts vary by lender, term length, and your credit profile.

3. Total Cost of the Loan

Understanding the total repayment amount is just as important as knowing your monthly payment. Even if the payment fits into your budget, it’s critical to assess:

- The APR (Annual Percentage Rate)

- Any origination or processing fees

- Late fees or prepayment penalties

Most reputable direct lenders are transparent about these costs and present them upfront before you accept the offer. If a lender avoids disclosing these details, it may be a red flag.

4. Early Repayment and Flexibility

Many online direct lenders allow you to repay your loan early without penalty. This can help reduce the total interest you pay and close out the loan ahead of schedule. Always ask whether early payment is allowed and whether it affects your repayment calculation.

5. Missed Payments and Late Fees

If you’re unable to make a payment on time, some lenders offer grace periods or repayment options—but not all do. Failing to make payments may result in:

- Additional late fees

- Impact on your credit (if reported)

- Difficulty qualifying for future loans

If you’re concerned about repayment, contact your lender early to discuss options.

Good Expert Tip

Before signing your loan agreement, review the full repayment schedule and total cost—not just the monthly amount. Responsible borrowing means knowing exactly what you’re agreeing to and planning ahead for every payment.

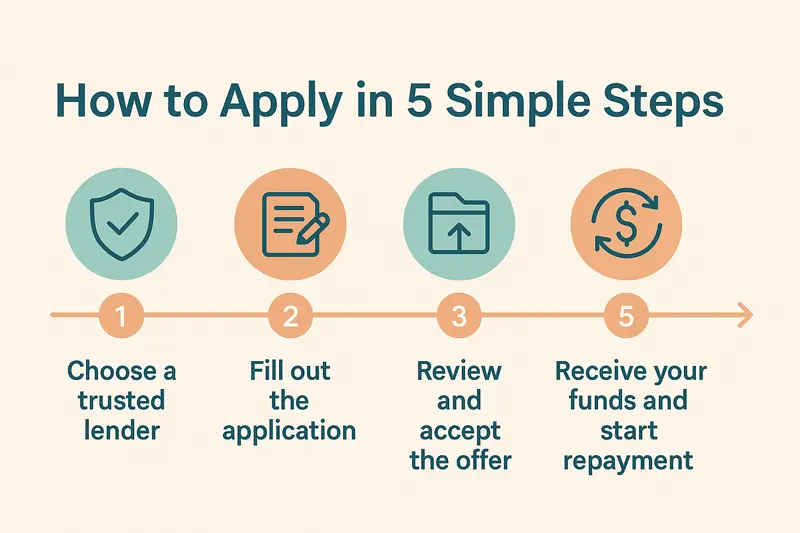

How to Apply for a $1000 Installment Loan Online

Applying for a $1000 installment loan online is designed to be straightforward, especially when working with a reputable direct lender. The process typically takes just a few minutes, and decisions are often made the same day. While each lender may vary slightly, the core steps remain the same—and being prepared can help speed things up.

- Start with a Trusted Lender

Choose an online direct lender with transparent terms, secure data practices, and clear contact information. Look for reviews, licensing disclosures, and an explanation of loan fees before filling out the application. Avoid sites that promise guaranteed approval or don’t explain how repayment works.

- Complete the Online Application

You’ll be asked to provide basic information, including:

- Full name and contact details

- Government-issued ID (such as a driver’s license or state ID)

- Proof of income (pay stubs, benefit letters, or bank statements)

- Active checking account details for deposit and repayment

Most applications include a soft credit check that won’t affect your score. This helps lenders evaluate your eligibility without causing any harm to your credit report.

- Review the Loan Offer

If you’re approved, the lender will present a loan offer outlining:

- The total amount borrowed

- Repayment schedule and due dates

- Interest rates and fees

- Total repayment amount

Take your time reviewing the terms. Make sure you understand the monthly payment amount, how long the loan lasts, and whether there are any fees for late payments or early repayment.

- Accept the Offer

Once you’re comfortable with the terms, you can accept the offer electronically. Many lenders provide a digital agreement that you can sign securely online.

- Receive the Funds

After accepting, funds are typically deposited into your checking account as soon as the next business day. In some cases—especially with early-day approvals—same-day funding may be possible, though it’s not guaranteed.

- Begin Scheduled Repayments

Repayment usually starts on your next payday or within 14 to 30 days, depending on your chosen schedule. Most lenders offer automatic withdrawals from your bank account to ensure you never miss a due date.

Good Expert Tip

Always save a copy of your loan agreement and repayment schedule. If anything changes with your income or ability to repay, contact your lender immediately to discuss options—communication is key to avoiding late fees or credit damage.

Choosing the Right Direct Lender

Not all lenders are the same—especially when you’re applying online. Choosing a trustworthy direct lender is just as important as understanding the loan itself. A responsible lender will provide clear, honest terms, protect your personal information, and make it easy to ask questions or get support throughout the process.

Here are a few key factors to help you choose the right provider for your $1000 installment loan:

1. Transparency of Loan Terms

A reputable lender will clearly outline:

- The total cost of the loan

- Payment amounts and due dates

- Interest rates and applicable fees

- Prepayment or late payment policies

If these details are vague or hidden in fine print, it may be a sign to look elsewhere. Responsible lenders prioritize clarity to help borrowers make informed decisions.

2. Direct Lending vs. Loan Brokers

Working with a direct lender means you’re borrowing from the same entity reviewing and approving your application. This often leads to faster processing and better communication. Brokers, on the other hand, may pass your information to multiple lenders, which can lead to unexpected outreach or varying loan terms.

If you prefer consistency and privacy, applying directly with a lender can offer more control and fewer surprises.

3. Secure Application Process

Your personal and financial details should always be protected. Look for:

- SSL-secured websites (check for the padlock in the browser)

- Privacy policy disclosures

- Clear explanations of how your data is used

Avoid lenders that don’t explain how they protect your information or that ask for unnecessary personal data.

4. Customer Support and Accessibility

Even if the loan process is fully online, it’s important to have access to real support. Check whether the lender offers:

- Phone or live chat support

- An FAQ section or help center

- Timely responses to inquiries

Lenders that are hard to reach before you borrow will likely be harder to work with if any issues arise later.

5. Online Reputation

Search for verified reviews, Better Business Bureau ratings, or feedback from actual customers. Be cautious of fake reviews or overly positive testimonials without substance.

Look for patterns in complaints—especially related to surprise fees, aggressive collection practices, or poor customer service.

Good Expert Tip

Before committing to a loan, take five minutes to read through the lender’s full website—not just the application page. A transparent lender will make it easy to find answers and understand your rights as a borrower.

Alternatives to $1000 Installment Loans (When to Consider Them)

While $1000 installment loans offer a structured and flexible borrowing option, they may not be the right fit for everyone. Depending on your financial situation, credit profile, or the urgency of your needs, you might want to explore other solutions before committing to a new loan.

Here are several alternatives that could serve you better depending on your circumstances:

1. Borrowing from a Local Credit Union

If you’re a member of a credit union, you may qualify for a small personal loan with lower interest rates and more favorable terms. Credit unions often work with members who have less-than-perfect credit and prioritize community lending practices.

However, these loans can take longer to process and may require more paperwork or a credit pull.

2. Negotiating Payment Plans with Service Providers

If you’re facing a utility bill, medical expense, or rent shortfall, consider speaking directly with the provider. Many companies are willing to set up payment plans or offer temporary relief if you’re upfront about your financial situation.

This can help you avoid borrowing entirely or reduce the amount you need.

3. Using an Emergency Fund (If Available)

If you’ve built up even a small emergency savings account, this may be the right time to use it. An emergency fund is designed for exactly these moments—when an unexpected cost arises and you need to bridge a gap without taking on new debt.

4. Community or Employer Assistance Programs

Some employers offer paycheck advances or short-term hardship loans. Local nonprofits and community programs may also provide emergency grants or interest-free loans to help with essentials like housing, utilities, or transportation.

These programs aren’t always widely advertised, so you may need to ask directly or check with local service organizations.

5. Credit Card Use (With Caution)

If you have access to a credit card with a manageable interest rate, it may be a convenient option—especially for smaller expenses. However, revolving credit can quickly lead to long-term debt if not paid off in full. Only consider this option if you’re confident you can repay the balance quickly.

While $1000 installment loans are a solid option for many, exploring these alternatives first can help you make a more informed financial decision and potentially avoid taking on unnecessary debt.

Good Expert Tip

If you’re unsure whether a loan is the best route, take 24 hours to evaluate your options. A short delay won’t solve the problem—but it may give you enough time to discover a better solution.

Conclusion

When managed wisely, $1000 installment loans can offer the flexibility and structure needed to handle unexpected expenses without falling into financial instability. With fixed payments, clear terms, and faster access to funds than traditional bank loans, they’re a practical solution for borrowers who need short-term support.

Still, the key to borrowing responsibly lies in choosing a transparent lender, understanding the full repayment schedule, and only taking out what you truly need. These loans work best when they’re part of a broader financial plan—not a quick fix used repeatedly.

If you’re considering applying, take time to compare your options, review your budget, and be honest about your repayment ability. Making informed decisions today can help you avoid unnecessary stress tomorrow.

Key Takeaways: $1000 Installment Loans

- $1000 installment loans are short-term, fixed-amount loans that offer predictable monthly or biweekly repayment schedules, making them easier to manage than lump-sum payday loans.

- These loans are ideal for covering urgent expenses such as car repairs, utility bills, rent gaps, or medical costs—especially when immediate cash flow is limited.

- A wide range of borrowers can benefit, including gig workers, renters, and individuals with fair or poor credit, provided they have a consistent source of income.

- Qualifying typically requires basic documents: proof of income, a valid state ID, and an active checking account. Many lenders use soft credit checks that won’t impact your credit score.

- Repayment terms are clear and fixed, allowing borrowers to plan their budgets. Terms usually range from 2 to 6 months, depending on the lender and payment frequency.

- Applying online is simple: fill out the application, review the loan terms, accept the offer, and receive funds—often by the next business day.

- Choosing a reputable direct lender is essential. Look for transparency in fees, security in the application process, and responsive customer support.

- Alternatives to installment loans—such as payment plans, emergency funds, or community assistance—may be better for some borrowers, depending on the situation.

- Reviewing all loan details before accepting an offer ensures you borrow responsibly and avoid unnecessary debt or unexpected charges.

Frequently Asked Questions

1. Can I get a $1000 installment loan with bad credit?

Yes, many direct lenders offer $1000 installment loans to borrowers with fair or bad credit. Approval often depends more on your income stability and ability to repay than your credit score. Some lenders use soft credit checks that don’t affect your score.

2. How long does it take to get a $1000 installment loan?

In most cases, funds are deposited within one business day after approval. If you apply early and your documents are verified quickly, same-day decisions are possible, though funding typically occurs the next day.

3. Will applying for a $1000 installment loan affect my credit score?

Most lenders perform a soft credit check during the application, which does not impact your credit score. However, missing payments after funding may be reported to credit bureaus and could negatively affect your credit profile.

4. What are the typical repayment terms for a $1000 installment loan?

Repayment terms usually range from 2 to 6 months, with fixed payment amounts. The exact term depends on the lender and your repayment preferences (monthly or biweekly). All terms are disclosed before finalizing the loan.

5. Are $1000 installment loans safe to apply for online?

Yes—when using a reputable, licensed direct lender. Always look for secure websites, clear disclosures, and transparent loan terms. Avoid sites that promise guaranteed approval or ask for unnecessary personal information upfront.

Get Personal Loans up to $1200

Get an Installment Loan to cover your Unexpected Expenses.

You can get up to $1,200 as soon as the next business day.