Easy Approval Installment Loans – Clear Terms, Trusted Process

- Installment Loans

When unexpected expenses pop up, getting access to extra funds quickly can make a real difference. That’s where easy approval installment loans may come into play—designed to offer a streamlined application process and faster lending decisions. But while the term “easy approval” may sound appealing, it’s important to understand what it truly means—and what it doesn’t.

Unlike payday or guaranteed loans that often come with risky terms, installment loans involve a set repayment schedule with fixed payments, making them a more manageable borrowing option for many. However, approval isn’t automatic. Lenders still review key factors like your income, financial history, and ability to repay the loan. That’s why it’s crucial to approach borrowing with clear expectations and a focus on responsible use.

In this guide, we’ll break down how easy approval installment loans work, who may qualify, what to watch for, and how to apply safely. Whether you’re dealing with medical bills, car repairs, or another pressing expense, this post will help you make informed, confident decisions.

Written by the Good Loans Fast Team: Our editorial team brings financial insights built on years of experience in short-term lending. We focus on responsible borrowing strategies, especially for those with less-than-perfect credit. All content is reviewed regularly to ensure accuracy and compliance with industry guidelines.

Good Loans Fast is a licensed Tribal lender offering installment loans to eligible borrowers. We are wholly owned by the Wakpamni Lake Community Corporation (WLCC), a tribal entity governed by the laws of a federally recognized tribe. Our team is committed to transparent, responsible lending that prioritizes access to fair financial solutions. You can view our licensing details here.

Disclaimer: This article is for general informational purposes only and does not constitute financial or legal advice. Loan terms, eligibility, and approval may vary based on underwriting review. We recommend consulting with a licensed financial professional before making borrowing decisions.

This content was created with the assistance of AI and reviewed by our editorial team to ensure accuracy, clarity, and compliance with responsible lending standards.

What Are Easy Approval Installment Loans?

When people hear the phrase “easy approval installment loans,” it’s easy to assume it means anyone can get one without hassle. But these loans are not guaranteed or risk-free—they’re just structured to be more accessible and streamlined than traditional bank loans.

Understanding the Term: “Easy Approval”

In a compliant and responsible context, “easy approval” simply means the application process is simplified and faster than many other lending options. Online forms, same-day decisions, soft credit checks, and minimal paperwork contribute to this perception.

However, lenders still evaluate key factors like:

- Your income and employment stability

- Your ability to repay the loan

- Your recent credit behavior (often via a soft credit check)

This is not a shortcut to guaranteed funding—responsible lenders still conduct due diligence to protect both parties from taking on unmanageable debt.

What Makes It an Installment Loan?

An installment loan refers to a type of loan repaid in equal payments over time, usually with a fixed interest rate and a clearly defined repayment schedule. Unlike payday loans or revolving credit, these loans:

- Have a predictable monthly payment

- Come with a fixed repayment term (e.g., 3 to 12 months)

- Do not require full repayment by the next paycheck

- May be available to borrowers across a wider range of credit scores

This structure gives borrowers more financial control and often lower risk of default when managed responsibly.

Designed for Flexibility and Convenience

Most easy approval installment loans are offered online, which helps speed up the process. Applicants can usually submit documents, verify income, and receive a lending decision within hours—sometimes even on the same day.

Still, speed should never replace scrutiny. Understanding your loan terms, fees, and repayment schedule is essential.

Good Expert Tip

“Easy” doesn't mean automatic. A soft credit check can still reveal patterns that affect approval, so always apply honestly and review the loan terms thoroughly before committing.

Who Can Qualify for Easy Approval Installment Loans?

Qualifying for an easy approval installment loan often feels more straightforward than applying for traditional bank credit—but that doesn’t mean every application is accepted. Lenders use a set of flexible but responsible criteria to determine who can reasonably manage repayment. This approach helps widen access to credit without bypassing essential risk assessments.

Key Qualification Factors

While every lender sets their own guidelines, the following factors are typically evaluated during the approval process:

- Verifiable Income

Lenders need to confirm that you have a reliable source of income—whether it’s from employment, self-employment, government benefits, or other consistent earnings. This demonstrates your ability to repay the loan on schedule. - Active Checking Account

An open and active checking account is often required, as it allows the lender to deposit funds and set up automatic repayments. It also helps verify financial stability. - U.S. Residency and Legal Age

Applicants must typically be legal residents and at least 18 years old. Proof of identity—such as a state-issued ID—is usually required. - Soft Credit Check Review

Although these loans may be available to borrowers with less-than-perfect credit, most lenders still conduct a soft credit check. This allows them to assess recent credit behavior without affecting your score. They may review your payment history, debt-to-income ratio, and other relevant data points. - Debt Load and Repayment History

Some lenders look at your overall financial profile—not just your credit score. A history of timely payments, low recent delinquencies, and manageable outstanding debt can all support approval.

Accessibility for a Range of Credit Types

One of the reasons these loans are appealing is that they may be accessible to borrowers with fair or poor credit—not just those with high FICO scores. However, that accessibility doesn’t eliminate risk. Approval is never guaranteed, and loan terms may vary depending on your financial profile.

Good Expert Tip

Lenders want to approve borrowers who can repay without hardship. Be honest in your application and choose a loan amount that fits comfortably within your monthly budget.

Benefits of Easy Approval Installment Loans

While no loan is risk-free, easy approval installment loans can offer several practical advantages—especially for borrowers who may not qualify for traditional credit options. These benefits go beyond the speed of the application process and extend to how the loan is structured, repaid, and used.

Fixed Payments Offer Predictability

One of the key advantages of installment loans is the ability to repay the borrowed amount through fixed, scheduled payments. This structure makes it easier to budget, since you’ll know exactly how much is due and when, unlike revolving credit or balloon-style repayment loans.

Predictability helps prevent surprises—so you can plan your finances without constantly adjusting for changing payment amounts.

Flexible Access Across Credit Types

Because most lenders conduct a soft credit check, installment loans with easier approval criteria are sometimes accessible to borrowers with fair or even poor credit. While approval is not guaranteed, lenders may be willing to work with a broader range of credit profiles if income and repayment ability are strong.

This makes these loans a potential fit for people who need access to funds but want to avoid high-risk products like payday or auto title loans.

Convenient Online Application Process

Many easy approval installment loans are offered through online direct lenders, which means:

- No need to visit a physical location

- Fast form submission and document upload

- Decisions often within hours—not days

This convenience is especially helpful for people managing urgent expenses or those with limited mobility or transportation.

Lower Stress Than Lump-Sum Repayment Loans

Unlike payday loans, which often require full repayment within two weeks, installment loans allow you to spread the cost over a longer period—typically several months. This reduces repayment pressure and can help avoid rolling over debt or falling behind on payments.

Transparent Terms (When Working with Reputable Lenders such us Good Loans Fast)

Responsible lenders will provide a clear breakdown of:

- Loan amount

- Repayment schedule

- Annual Percentage Rate (APR)

- Total repayment cost

- Any applicable fees

Understanding these details upfront creates greater financial transparency and allows borrowers to make more informed decisions.

Good Expert Tip

The true benefit of an installment loan isn’t just in quick access—it’s in how well the terms match your financial capacity. Focus on affordability, not just speed.

Responsible Borrowing: What “Easy Approval” Doesn’t Mean

The phrase “easy approval” often gives the impression that installment loans are available to anyone without concern for credit history or repayment ability. While the process may be faster and more accessible than traditional bank loans, it’s essential to recognize that these loans still carry financial responsibility. Misunderstanding this can lead to poor borrowing decisions and long-term financial consequences.

“Easy” Refers to Process—Not Risk-Free Lending

Lenders that offer easy approval installment loans typically streamline the application process. This may include:

- Simple online forms

- Minimal documentation

- Same-day decisions

- Soft credit checks

However, these features do not eliminate the lender’s obligation to assess risk—or your obligation to repay. Every legitimate lender still evaluates a borrower’s ability to make on-time payments. That evaluation helps protect borrowers from taking on debt they cannot manage and ensures the lender is practicing responsible lending.

Approval Is Never Guaranteed

Some borrowers mistakenly interpret “easy approval” as a promise that anyone will be approved, regardless of financial circumstances. This is not the case. Lenders still require:

- Verifiable income

- An active checking account

- Legal identification

- Satisfactory credit behavior or stability

If a lender promises guaranteed approval, it’s a red flag and often a tactic used by scams or predatory operations. Responsible lenders provide access—not automatic acceptance.

Borrow Only What You Can Repay

Easy application doesn’t mean easy repayment. Even small installment loans require consistent, on-time payments over a set term. Late or missed payments may lead to:

- Late fees

- Negative marks on your credit report

- Additional interest accrual

- Collection activity in severe cases

Before applying, review your budget and determine whether the monthly payment will be manageable alongside your existing obligations. Responsible borrowing involves planning for repayment—not just focusing on fast access to cash.

Good Expert Tip

Ask yourself this before applying: “Can I afford the monthly payments without cutting into essentials?” If the answer isn’t a confident yes, take time to reassess your needs or consider smaller loan amounts.

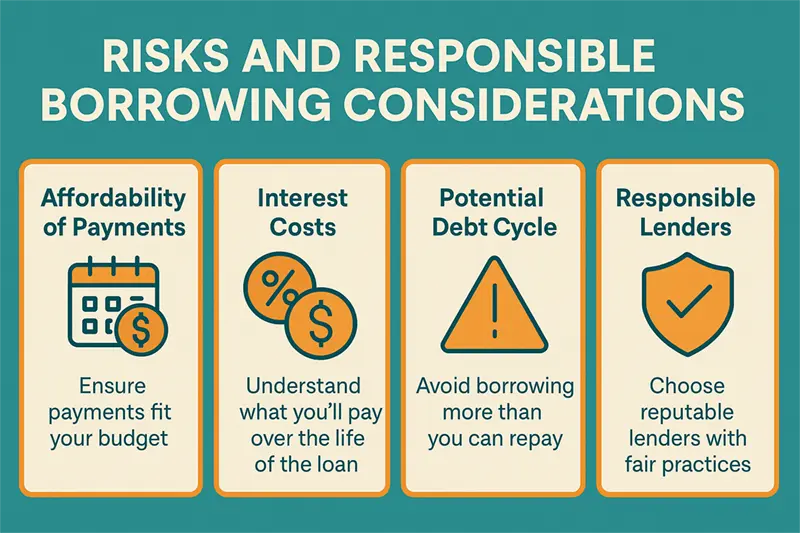

Risks and Responsible Borrowing Considerations

Even when offered through reputable lenders, easy approval installment loans come with financial obligations that should not be overlooked. Borrowing money—especially under time pressure or financial stress—can lead to costly consequences if the decision isn’t made carefully. Understanding the risks before applying is a crucial part of responsible financial behavior.

Debt Can Accumulate Quickly

One of the most common risks with installment loans is borrowing more than you can afford to repay. Because the approval process may be faster and more accessible, some borrowers take out loans without fully calculating how it will impact their monthly budget.

If you already have existing financial obligations, even a modest monthly installment could stretch your finances too thin, leading to late payments, overdraft fees, or increased credit card usage.

Missed Payments Affect More Than Just Fees

Missing a payment isn’t just a minor inconvenience—it can lead to a cascade of consequences. These may include:

- Late payment fees that increase your total loan cost

- Damage to your credit report if the lender reports to credit bureaus

- Strain on your ability to qualify for future credit

- Increased stress or pressure on your personal finances

Some borrowers also make the mistake of delaying payments on other bills to prioritize loan payments, leading to a cycle of short-term fixes and long-term instability.

Longer Terms Can Mean Higher Costs

While spreading out payments may seem easier on your budget, a longer repayment term can increase the total cost of borrowing due to accumulating interest. A loan with a 10-month term may have a lower monthly payment than one with a 4-month term—but you might pay significantly more in total by the end of the agreement.

It’s important to strike a balance between manageable payments and minimizing interest paid over time.

Short-Term Fixes Can Lead to Long-Term Dependence

Installment loans can be helpful in emergencies—but they’re not designed to solve ongoing financial shortfalls. Relying on loans to cover regular expenses, such as rent or groceries, is often a sign of a deeper budget issue that needs attention. Repeated borrowing can lead to loan stacking or dependency, which increases financial risk and stress over time.

Good Expert Tip

Before applying, create a simple repayment plan. Map out how the loan will fit into your existing income and expenses for each month of the term. If the numbers don’t work comfortably, reconsider the amount—or whether the loan is necessary at all.

Watch Out for Scams and Unrealistic Promises

The term “easy approval” is often misused by scammers and predatory lenders to lure borrowers into risky, costly, or outright fraudulent loan agreements. When you’re under financial pressure, it’s easy to be drawn to offers that seem fast, effortless, or guaranteed. But in lending—especially online—if something sounds too good to be true, it usually is.

Red Flags to Avoid

Here are several common signs that a lender or loan offer may be unsafe:

- Guaranteed Approval with no review of your financial background

- No Credit Check, No Documents Required, and no income verification

- Upfront Fees required before you receive funds

- Unsecured Websites (missing “https” or a padlock icon)

- Vague or Missing Disclosures about interest rates, total repayment amount, or late fees

- High-pressure tactics that push you to act immediately

Reputable lenders do not promise approval without an application review, and they never ask for payment before releasing loan funds.

How to Verify a Lender’s Legitimacy

Before sharing any personal or financial information online, take these steps to confirm the lender is legitimate:

- Check for State Licensing or Tribal Affiliation: All legitimate lenders are either licensed to operate or legally authorized under tribal lending laws.

- Search for Verified Contact Information: A real company will have a working customer service number, physical address, and professional website.

- Read Reviews and Complaints: Look for recent feedback online or check if the lender is listed with consumer protection organizations or regulators.

- Avoid Offers Received by Text or Social Media DMs: These are common scam channels.

Be Skeptical of Unsolicited Offers

Scammers often target individuals who are actively searching for loans online. You may receive emails or texts that seem legitimate at first glance but lead to phishing pages or fake loan applications designed to harvest your personal data.

If you receive an offer you didn’t request—especially one promising instant funds—approach it with caution. Do not click any links or provide your information until you’ve verified the sender and reviewed the offer carefully.

Good Expert Tip

A legitimate lender will never guarantee approval without checking your financial profile. If a loan offer skips over basic requirements or demands money upfront, walk away—it’s likely a scam.

How to Apply for Easy Approval Installment Loans

Applying for an easy approval installment loan is typically faster and more straightforward than applying for traditional credit. While approval is never guaranteed, the process is designed to reduce unnecessary steps and help qualified applicants get decisions quickly—often within the same day. However, it’s still important to follow each step carefully and submit accurate, verifiable information.

Step 1: Choose a Reputable Lender

Start by selecting a lender that is transparent, licensed, and clearly outlines the loan terms. Avoid lenders that advertise “guaranteed approval” or require upfront fees. A trustworthy lender will display:

- Loan amounts, rates, and terms clearly

- State licensing or tribal affiliation

- Customer support contact options

- Secure application pages (https)

Look for customer reviews or third-party verification if you’re unsure about a provider.

Step 2: Complete the Online Application

Once you’ve chosen a lender, begin the application on their official website. You’ll usually be asked to provide:

- Your full name and contact information

- Proof of income (pay stubs, benefits, or bank statements)

- Employment status and monthly earnings

- A valid state-issued ID

- Bank account details for fund deposit and repayments

Many lenders conduct a soft credit check, which won’t affect your credit score but helps assess your ability to repay the loan.

Step 3: Review the Loan Terms Carefully

If approved, the lender will present a loan agreement outlining:

- Loan amount

- Repayment schedule

- Annual Percentage Rate (APR)

- Total repayment amount

- Fees for late or missed payments

Take time to review every detail—even if the offer feels urgent. Don’t move forward until you’re confident that the loan fits your budget.

Step 4: Accept the Offer and Receive Funds

After signing the agreement electronically, funds are typically deposited directly into your bank account—sometimes as soon as the next business day. Be sure to monitor your account and retain a copy of the loan agreement for your records.

Good Expert Tip

Only apply for one loan at a time. Submitting multiple applications with different lenders can complicate your finances and lead to unnecessary confusion—even if soft checks are used.

How to Compare Lenders Offering Easy Approval Installment Loans

Not all lenders who advertise easy approval installment loans follow the same standards. Some prioritize speed and convenience, while others may focus on flexible terms or lower costs. Comparing lenders helps ensure you’re not only getting access to funds but also choosing a loan that aligns with your financial needs and repayment ability.

Making an informed decision can protect you from unexpected fees, confusing terms, and poor customer service—especially when applying online.

Look for Transparent Loan Terms

A reputable lender will present all essential loan information up front, before you sign anything. Look for clear answers to these questions:

- What is the total loan amount being offered?

- What is the APR (Annual Percentage Rate), and how does it affect total repayment?

- Are there late fees, prepayment penalties, or other charges?

- What is the exact repayment schedule (e.g., monthly, biweekly)?

- How long is the loan term?

If any of this information is missing or unclear, proceed with caution. Vague or buried terms are a sign the lender may not be acting in your best interest.

Assess the Lender’s Reputation

Before submitting an application, take a moment to research the lender. You can:

- Read recent customer reviews on trusted third-party sites

- Search for any complaints with consumer protection agencies

- Verify that the lender is either state licensed or affiliated with a recognized tribal lending entity

- Check for a working customer service number and support options

Responsible lenders are easy to reach, answer questions clearly, and have a track record of fair lending practices.

Prioritize Lenders That Offer Soft Credit Checks

If you’re comparing options, prioritize lenders that use a soft credit check during the application process. This allows you to explore eligibility without damaging your credit score. However, also confirm whether a hard credit inquiry will be performed if you decide to move forward with the loan.

Watch for Added Value or Support

Some lenders may offer features that improve the overall borrowing experience, such as:

- Flexible payment dates

- Grace periods

- Online account access

- Educational resources or budgeting tools

These extras can indicate a lender that prioritizes long-term customer relationships rather than just transactional lending.

Good Expert Tip

Don't just compare monthly payments—compare the total cost of the loan. A lower monthly payment may seem attractive, but a longer term with more interest can cost you significantly more in the end.

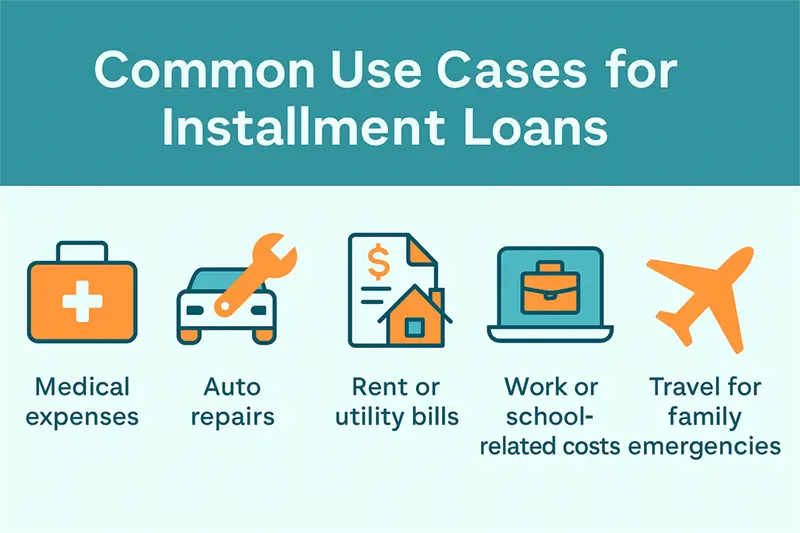

Common Use Cases for Installment Loans

Easy approval installment loans are often used to cover urgent or essential expenses that can’t wait for a future paycheck. Their structured repayment format makes them a practical solution for short-term financial gaps—especially when budgeting and stability are top priorities.

Because the application process is faster and often more accessible, borrowers turn to installment loans for a variety of everyday needs—not luxury purchases or long-term financing.

Emergency Medical Expenses

Unexpected doctor visits, urgent care fees, dental work, or prescription costs can strain your budget. Installment loans can help cover these out-of-pocket expenses so you can get the care you need without delaying treatment due to cost.

Auto Repairs and Transportation Needs

When your car breaks down, waiting for payday isn’t always an option. Installment loans are commonly used to fund urgent repairs, tire replacements, or maintenance that keeps your transportation reliable and safe—especially for commuting to work or handling family responsibilities.

Rent, Utilities, or Essential Bills

Falling behind on rent or utilities can quickly lead to late fees, service interruptions, or housing instability. Installment loans may help bridge the gap for essential bills, giving you time to catch up without turning to higher-risk lending options.

School or Work-Related Expenses

Sometimes you need to cover the cost of school supplies, course fees, uniforms, or tools required for a job. An installment loan can offer short-term support while you invest in your education or employment.

Travel for Family Emergencies

Whether it’s an unexpected funeral, illness, or caregiving obligation, family-related travel can’t always be postponed. Installment loans may provide the flexibility to manage these time-sensitive trips without depleting your savings.

Good Expert Tip

Use installment loans for needs, not wants. Focus on expenses that support your health, income or stabilit, rather than optional or high-cost purchases that could lead to financial regret.

Conclusion

Easy approval installment loans can offer a practical and accessible solution for managing unexpected expenses—especially when time is limited and traditional financing isn’t an option. Their structured repayment terms, predictable monthly payments, and streamlined application process make them a valuable tool when used wisely.

But while the process may be simplified, responsible borrowing remains essential. Approval is never guaranteed, and each loan comes with the obligation to repay on time, in full, and within your means. Choosing a transparent, licensed lender and reviewing all terms before signing is critical to protecting your financial health.

When approached thoughtfully, installment loans can help you cover urgent costs without falling into cycles of high-risk debt or uncertainty. Use them as part of a broader financial strategy—not a quick fix—and always make sure the loan fits within your long-term budget.

Key Takeaways: Easy approval installment loans

- Easy approval installment loans are designed to offer faster access to funding through a simplified online application process, fixed repayment terms, and soft credit checks—but approval is never guaranteed.

- The phrase “easy approval” refers to convenience, not automatic acceptance. Lenders still evaluate income, financial behavior, and ability to repay to ensure responsible lending practices.

- Borrowers with varying credit histories may qualify if they meet core criteria such as steady income, a valid ID, and an active bank account. A soft credit check is often used to assess risk without impacting the applicant’s credit score.

- These loans can offer several benefits, including predictable monthly payments, flexible terms, and convenience—but they must be used wisely to avoid unnecessary debt or overextension.

- Responsible borrowing means understanding the loan terms, budgeting for repayment, and avoiding the temptation to borrow more than needed. Long repayment terms may lower monthly payments but often increase total loan cost.

- There are real risks involved, including potential late fees, damage to credit, and the risk of relying on installment loans as a recurring solution to financial gaps.

- Scams and predatory lenders often misuse the term “easy approval” to attract vulnerable borrowers. Always verify that a lender is licensed, transparent, and never asks for upfront fees or promises guaranteed funding.

- The application process typically includes verifying your identity, income, and bank account information. Reputable lenders provide clear terms before disbursement and do not pressure you to act immediately.

- When comparing lenders, look beyond the monthly payment. Focus on total loan cost, APR, and the presence of transparent disclosures. Prioritize lenders that use soft credit checks and offer responsive customer support.

Common use cases for installment loans include emergency medical bills, car repairs, essential bills, or travel related to family emergencies—not discretionary or luxury expenses.

Frequently Asked Questions

1. Are easy approval installment loans guaranteed?

No, easy approval installment loans are not guaranteed. While the application process may be more accessible and faster than traditional loans, lenders still evaluate your income, financial stability, and recent credit behavior before making a decision.

2. What credit score is needed for easy approval installment loans?

There’s no universal credit score requirement. Many lenders use a soft credit check and may consider applicants with fair or poor credit, if they can demonstrate the ability to repay through stable income and a verified bank account.

3. How fast can I get funds from an easy approval installment loan?

If approved, funds may be deposited as soon as the next business day. Exact timing depends on the lender’s processing schedule and your bank’s deposit policies.

4. Are easy approval installment loans safe?

Yes, when obtained from a licensed and transparent lender. Always check for clear terms, a secure website, and no upfront fees. Avoid offers that promise guaranteed approval or ask for payment before loan disbursement.

5. Can I apply for an installment loan with bad credit?

Yes, some lenders offering easy approval installment loans may work with applicants who have bad credit. Approval is still based on income, financial obligations, and the ability to repay—regardless of credit score

Get Personal Loans up to $1200

Get an Installment Loan to cover your Unexpected Expenses.

You can get up to $1,200 as soon as the next business day.